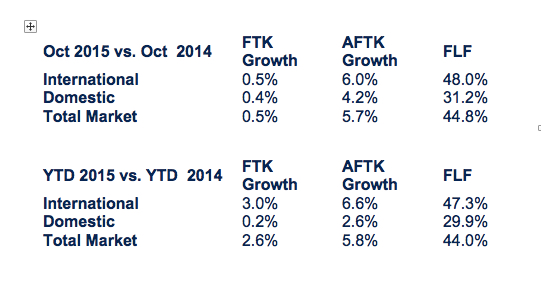

The International Air Transport Association (IATA) released data for global air freight markets showing that air cargo volumes measured by freight tonne kilometers rose just 0.5 per cent in October compared to a year ago. Year-on-year expansion fell back from September’s faster growth rate with total cargo volumes in October shrinking 1.1 per cent from the peak of the uptrend at the end of 2014.

European carriers have driven recent improvements in air cargo growth, but they ran out of steam in October with a rise of just 0.2 per cent. Other regions also underlined the weak October trend with he most significant decline in cargo activity was experienced by North American carriers, who reported a 2.4 per cent fall in volumes. Latin America (-8.1 per cent) and Africa (-1.1 per cent) are smaller markets and also declined. Asia-Pacific was up, little more than Europe with a rise of 0.3 per cent. Growth in the Middle East, although a robust 8.3 per cent, was some 4.3 percentage points down on the average performance for the year to date.

“The outlook for air cargo continues to be very difficult. While there was some optimism from third quarter growth it has all but disappeared as the industry basically flat-lined,” said Tony Tyler, IATA’s director general and CEO. “Cargo capacity has grown largely in lock-step with the continued robust demand for passenger travel. As a result, freight load factors have sunk to the 44 per cent range—a level not seen since 2009. Early signs of improvement in export orders may bode well for trade and air cargo but this is unlikely to prevent air cargo finishing 2015 on a low note,” said Tyler.

FTK comparisons

Regional analysis in detail

Asia-Pacific carriers saw a slight rise in FTKs of 0.3 per cent in October compared to October 2014, and capacity expanded 2.9 per cent. Trade growth in China and other key export economies remains disappointing. Chinese export orders, however, spiked in October, which could result in better demand for air freight in the next 2-3 months.

European carriers reported a rise in demand in October of just 0.2 per cent compared to a year ago and capacity rose 5.6 per cent. Although this is a weaker performance than in recent months, improvements in the Eurozone are expected to continue, especially trade activity to/from Central and Eastern Europe.

North American airlines experienced a decline of 2.4 per cent year-on-year and capacity grew 6.0 per cent. There are mixed signals from this market. Recent month-to-month results appeared to indicate a return to growth, but the latest manufacturing and export reports are poor. Strong demand for air freight in the coming months appears unlikely.

Middle Eastern carriers saw demand expand by 8.3 per cent, and capacity rise 11.6 per cent. Recent air cargo growth in the region continues to trend well below the rates seen for the first half of the year. Saudi Arabia and the UAE, among others in the region, have seen slowdowns in non-oil sectors, but growth rates remain robust enough to sustain solid demand for air cargo.

Latin American airlines reported a decline in demand of 8.1 per cent year-on-year, and capacity expanded 5.0 per cent. Year-to-date performance for Latin American air cargo is the worst of any region by some margin, contracting by 5.9 per cent. Air cargo demand appears to be mirroring weakening consumer sentiment in key regional economies.

African carriers experienced a fall in demand of 1.1 per cent, and capacity rose by 6.9 per cent. Despite the October result, Africa is still the second fastest growing air cargo market for the year-to-date. Demand is holding up despite the underperformance of Nigeria and South Africa.