Global air cargo was in its fourth straight month of growth in August as load factors jumped eight percentage points year on year, data from CLIVE Data Services and TAC Index showed.

The whole month’s volume was down 17 percent from a year ago which was a far cry from the 41 percent decline seen in April, when demand started to rally.

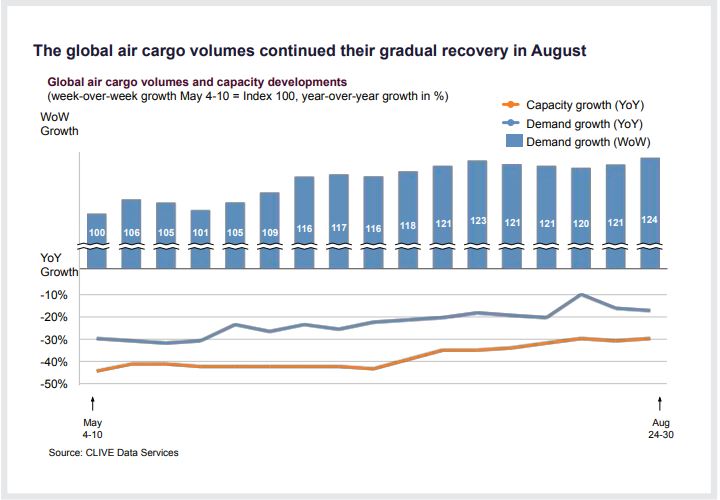

Air cargo volumes in the last week of August were four percent less than what were seen for the same period in 2019, putting off previous concerns of dried-up demand after the PPE peak.

CLIVE Data’s managing director, Niall van de Wouw, said the results were “not great, but by no means a disaster,” as the global dynamic load factor dropped two percentage points to 68 percent from July.

“The capacity crunch is still there but is becoming slightly less and, as a result, load factors and yields are going down and becoming closer to pre-COVID levels, even though they are still elevated,” he added.

“Airline cargo departments have never been in control of their own destiny, and they’re still not, but they are in control of the present and short term in deciding where to place their cargo capacity. Whereas cargo has often been regarded as the ‘freeloader’ of the airline industry because it has always been a by-product of far greater passenger revenues, right now it is passengers who are the ‘freeloaders’ because cargo is the main source of revenue for many airlines and helping to get passenger flights back into the air.”

The managing director does not expect passenger numbers to return soon but until then he says “air cargo will continue to have its day in the sun and combination carriers will have to hope this can sustain their slimmed down operations until passenger confidence and bookings return.”

Across the Atlantic, the westbound load factor fell to 82 percent in August from 88 percent in July, whilst the eastbound load factor slid seven percentage points to 65 percent over the same period.

CLIVE Data explained that figures for the Atlantic trade lane reflected the pressure on the dynamic load factor—based on both volume and weight of cargo flown and capacity available—of additional capacity entering the market.

Pricing also rolled back slightly from July. Whilst yields on the China-Europe route jumped 25 percent from a year ago with capacity 19 percent lower, pricing slipped 2.5 percent on this route. Yields on the transpacific lane or the China-US route climbed 35 percent, whilst pricing was down 5 percent.