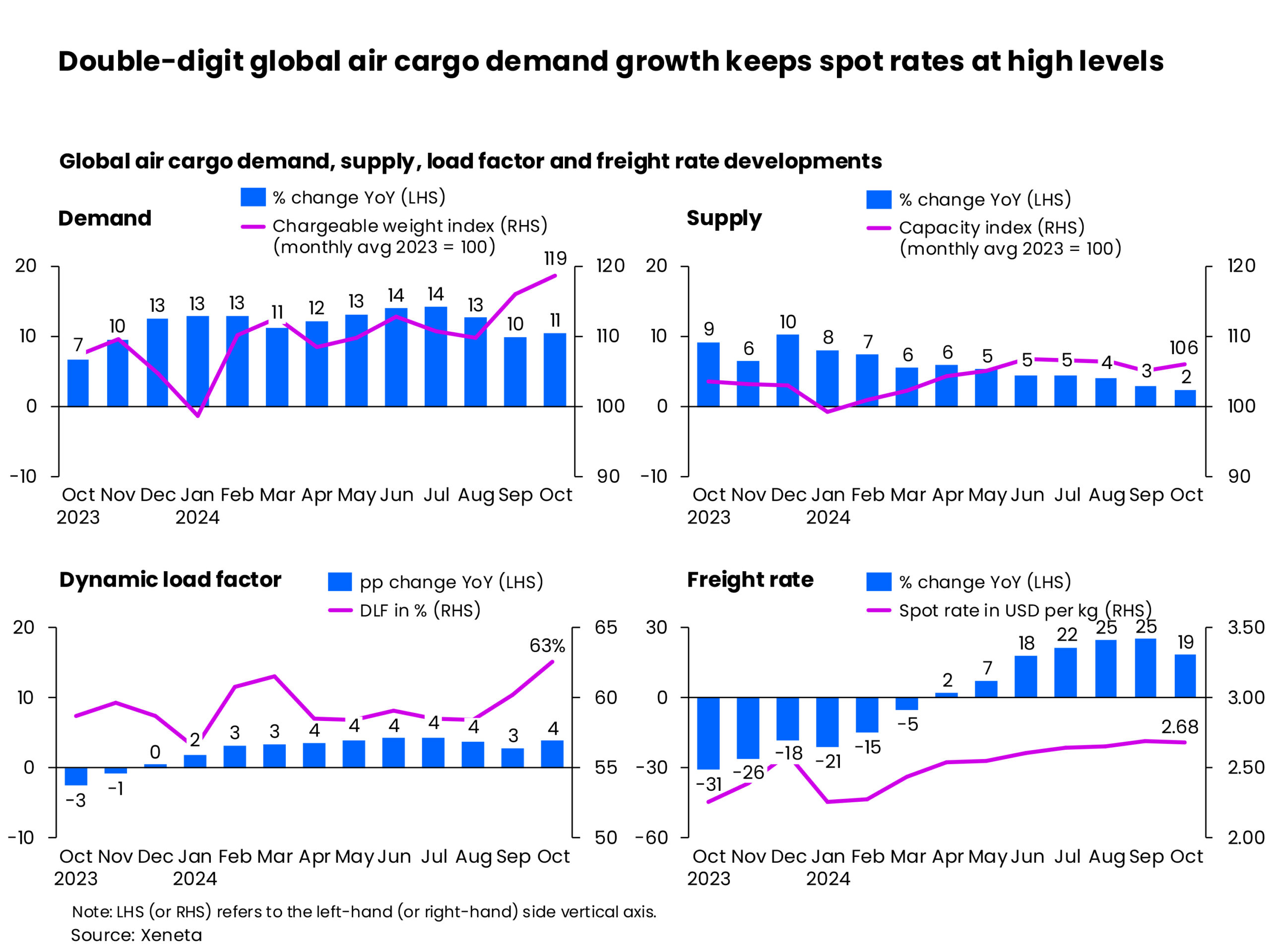

Not even zero growth in November and December can disrupt the global air cargo market from landing a year of unexpected double-digit demand growth in 2024. Healthy volumes of +11% in October and spot rates up +19% year-on-year reflected the growing maturity and balance among buyers and sellers of air cargo capacity, according to the latest market data by Xeneta.

A year of constant, unexpected disruptions outside of the industry’s control – which began with a growth forecast as per October 2023 of +1-2% for the full 2024 – is now firmly on course to end on a high in terms of demand. Such conditions traditionally result in winners and losers, but lessons learned and applied by shippers, freight forwarders, and airlines “shows the industry at its best,” says Niall van de Wouw, Xeneta’s Chief Airfreight Officer.

“The frequency and diversity of ‘storms’ coming the way of the air cargo industry in 2024 mean this year could have been quite messy, but the industry has found a way to navigate these challenges,” he said. “This shows the prep work has paid off as well as the flexibility shown in the industry. We see more emphasis on maintaining relationships than squeezing every last dime of revenue.”

While October’s global air cargo spot rate continued to stay elevated – averaging USD 2.68 per kg and just a few cents below 2023’s peak season high – the growth momentum slowed down from +25% in September, due mostly to a high comparison base in October 2023. In terms of the month-on-month trend, October’s spot rate was relatively flat compared to September.

The elevated year-on-year growth spot rate was supported by continued double-digit growth (+11%) in global demand, measured in chargeable weight. In comparison, global cargo capacity supply edged up only 2% year-on-year.

This supply and demand imbalance pushed the dynamic load factor up 4 percentage points to 63% in October. Dynamic load factor is Xeneta’s measurement of capacity utilisation based on volume and weight of cargo flown alongside available capacity.

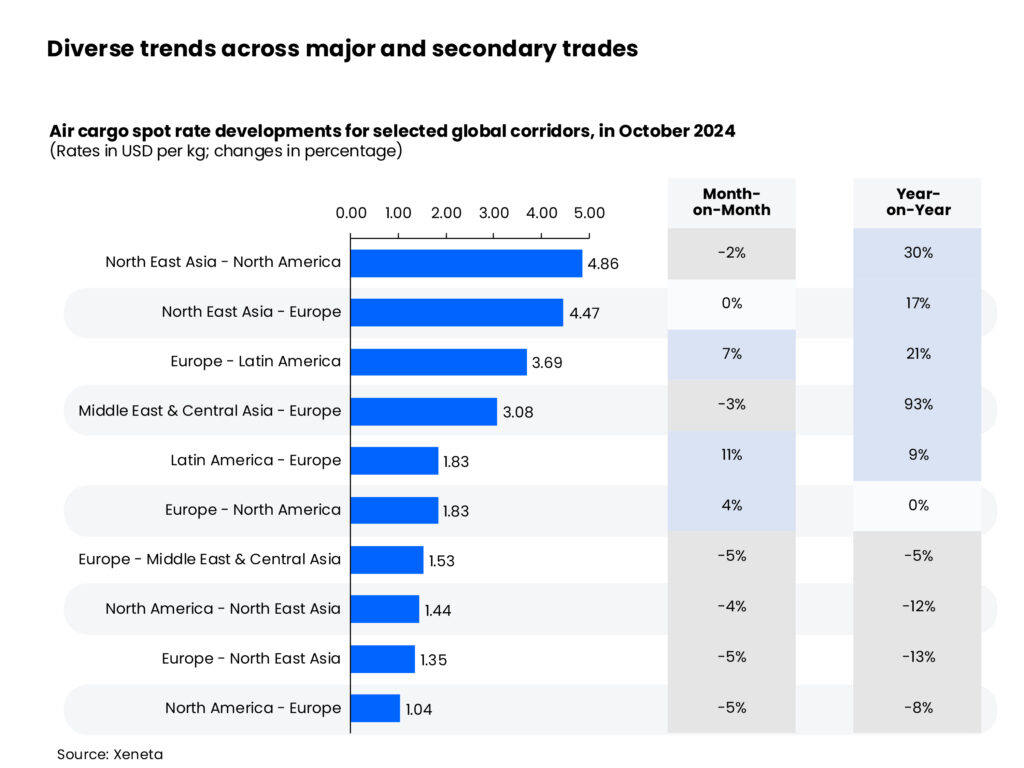

Zooming into the corridor level, Europe to North America saw the largest month-on-month volume increase of +11%. The return leg also saw a +10% month-on-month increase as shippers and forwarders took precautionary measures to lessen the impact of the 3-day strike by dockworkers at US East Coast and Gulf Coast ports. A quicker-than-expected resolution to this industrial action, however, saw the positive impact of the strike on air cargo volumes ebb away after reaching a peak in the week ending 20 October. Nonetheless, the rise in this corridor’s air cargo rates is likely to continue after airlines reduced cargo capacity at the end of the month to mark the start of winter schedules.

Capacity traditionally shifts to corridors generating higher revenues, which leads to a more balanced air cargo supply and demand. As a result, spot rates from Northeast Asia to North America, a top fronthaul corridor, stayed relatively flat month-on-month – in part due to a cooling down after a September boost caused by extreme weather disruptions and China’s Golden Week holidays.

Similarly, the Northeast Asia to Europe market stayed flat compared to a month ago. Despite several cancelled passenger flights between Europe and China due to uncompetitive routings, the corridor’s air cargo capacity still rose due to increased freighter capacity. This influx of capacity contributed to a decline in backhaul spot rates both month-on-month and year-on-year.

Shifting capacity to Asia from the Americas market also triggered freight rate increases in secondary corridors. Spot rates ex South America to Europe and its return leg rose by high single digits or double-digits month-on-month.

Middle East & Central Asia to Europe spot rates ticked down -3% month-on-month. Contributing factors included the easing of civil unrest in Bangladesh and subsiding weather disruptions.

“What we are seeing in the air cargo market is a compliment to the increasing ability of shippers, freight forwarders, and airlines to manage disruptions and process these kinds of volumes without as much drama around spiralling rates. Over the long-term, this is better for everybody,” van de Wouw said.

“There is a maturity in the market which stems from airlines being better prepared this year as well as there being clearer rules in place between shippers and forwarders, and forwarders and airlines. This is good for relationships – and good for consumers. Rates are still elevated versus a year ago, but despite strong demand, rising load factor, and only a modest increase in supply, they are not going crazy. Lessons have been learned and people are looking for healthy, reasonable rates on both sides.

“This puts air cargo demand safely on course to report double-digit growth in 2024, and not even zero growth in November or December is going to disrupt this,” he added.

The next level of market maturity, van de Wouw says, will be indexing between shippers and forwarders using a neutral third-party source to adjust rates through the duration of their contracts. “Indexing will benefit all parties and create confidence to enter long-term contracts. It is a natural next step in a market that is clearly seeing greater balance from better preparedness,” van de Wouw said.