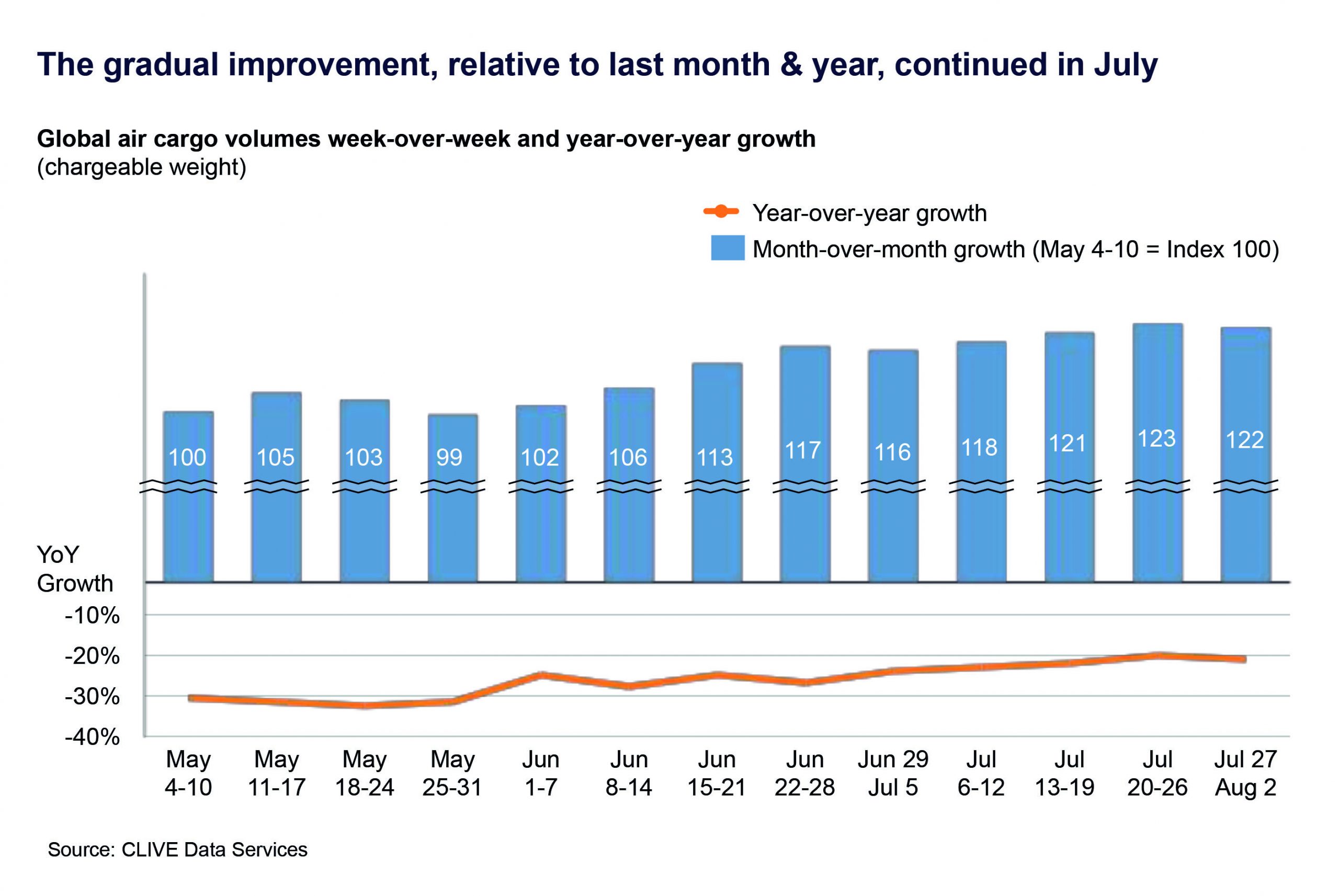

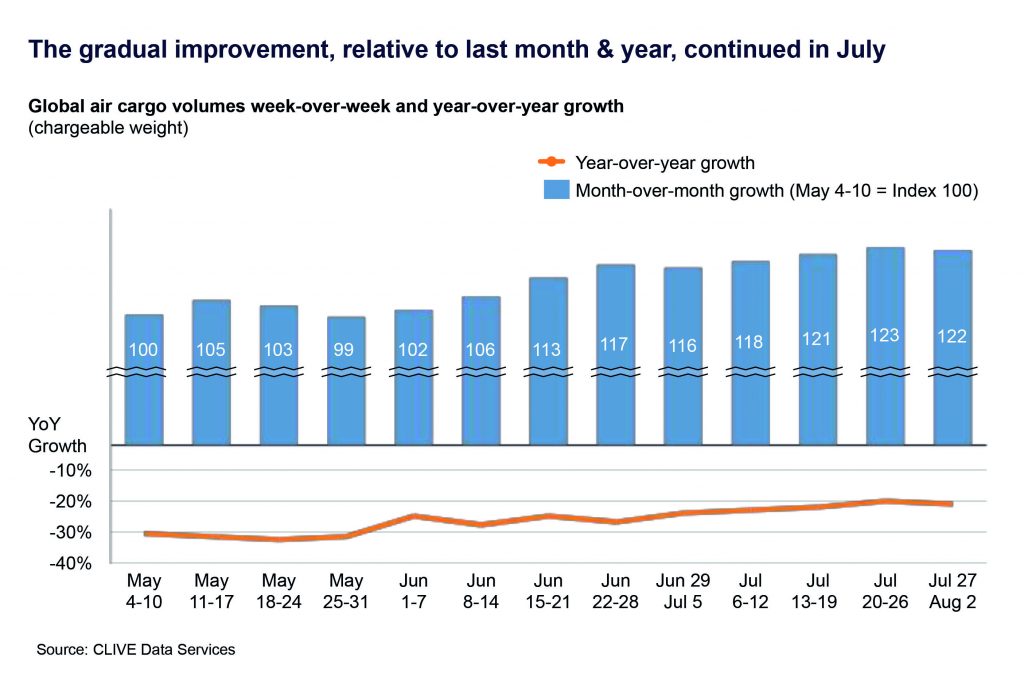

Latest market analysis from CLIVE Data Services shows that air cargo volumes continued to climb in July, inching up 8 percent over the previous month. Meanwhile, load factors for the month remained ahead of last year’s levels.

Air cargo volumes were down 20 percent year-on-year in July, but was an improvement compared to the drops in April (26 percent), May (31 percent) and June (37 percent).

Despite sliding 0.6 percent versus June, CLIVE’s dynamic load factor of 70 percent for July, based on both volume and weight terms of cargo flown and capacity available, was 8 percentage points higher than a year ago.

Niall van de Wouw, managing director at CLIVE Data Services, said, “Our market analyses for July, especially compared to what we were reporting a few months ago, shows the gradual but consistent climb up the slope to recovery for the air cargo market is continuing.”

Despite the gradual uptrend, van de Wouw noted that it’s not close to a ‘V’-shape recovery, but reassured that cargo volumes are showing some resilience.

“To put the 70 percent dynamic load factor into perspective, during the Christmas 2018 proper peak season it stood at 68%, and now we are in July, normally the doldrums summer period for the air cargo industry,” van de Wouw explained.

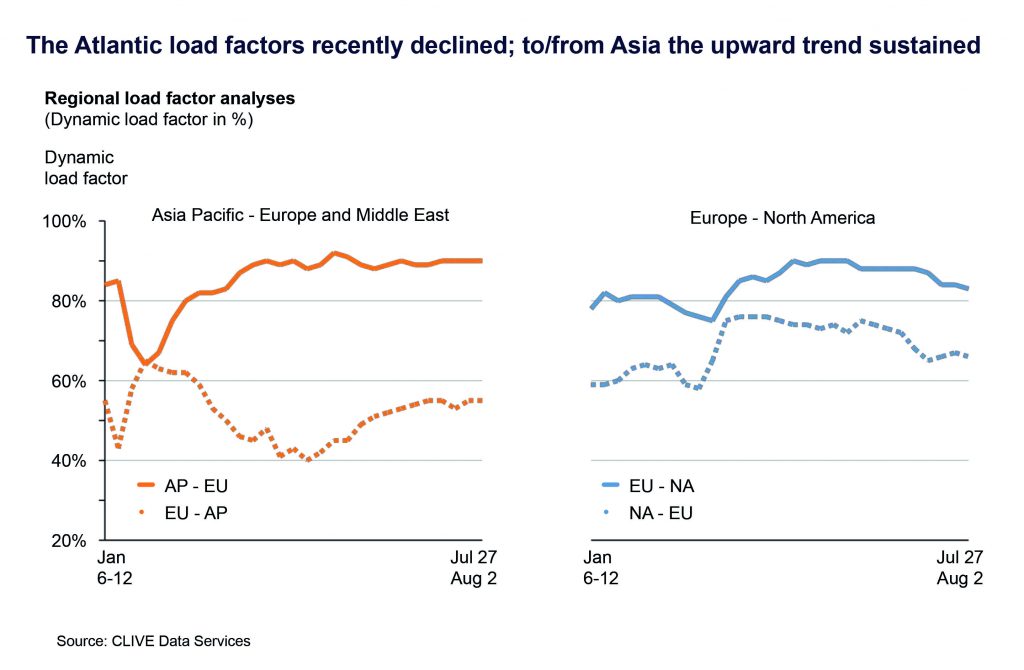

However, the managing director said that beneath the global average were regional differences. “The load factors to and from Asia show a different pattern than the ones across the Atlantic but this decline in load factor is mainly caused by increasing capacity. For example, Eastbound Atlantic capacity in the week of July 27-August 2 was 10% higher than in the last week of June, whilst cargo volumes rose by ‘just’ 4% over that same timeframe.”

‘Dynamic load factor’ year-on-year analyses for week 31 (July 27-August 2):

- 21 percentage point increase on the North America to Europe lane versus July 2019

- 19 percentage point increase on the Europe-North America lane

- 10 percentage point increase on the Asia-Europe & Middle East lane

- Closing the gap on the Europe & Middle East-Asia lane, 5 percentage point decline versus July 2019 but continually getting closer to the market level of 2019 after a ‘seismic fall earlier’ in the year