Photo credit: Gemma Evans on Unsplash

After some form of recovery to pre-pandemic levels in the first two months of the year, global volumes for the four full weeks of March 2021 were unable to continue the recovery seen in January and February, according to latest data from CLIVE Data Services and TAC Index.

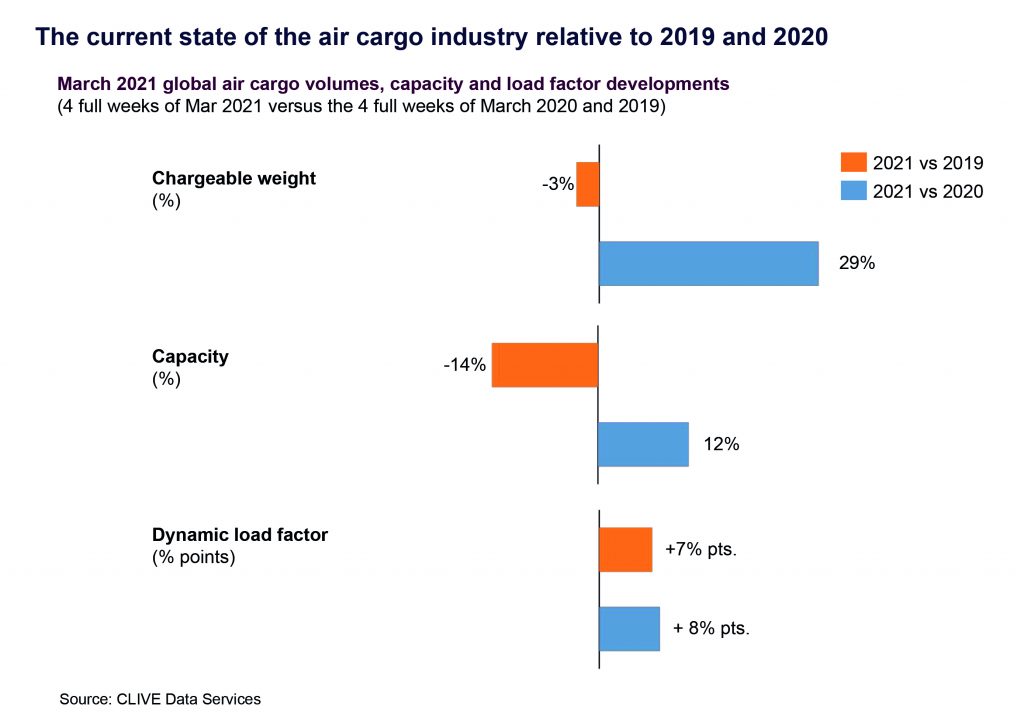

Volumes dropped 3 percent during these weeks and worsened towards the end of the month, sliding 4 percent week on week relative to the start of the month. Nonetheless, CLIVE Data says the air cargo market is in far better shape than a year ago when the outbreak of the Covid-19 virus led to a sudden collapse in global capacity, where more than half was wiped out from the skies and moved to storage lots in deserts or disposed. So numbers improved versus last year but down from two years prior. For context, volumes in March were 29 percent up over the same month 2020, peaking at 55 percent in the last two weeks. Niall van de Wouw, managing director of CLIVE Data Services, commented: “March data shows us the market is still very supply driven. After indicators that the global air cargo market was seeing some ‘light at the end of the tunnel’ in January and February after a year of such high disruption, this latest industry data will reign in that optimism slightly.”

De Wouw goes on to say, “This may reflect Covid-19 fatigue in the buying habits of businesses and consumers as we see more reports of infection rates creeping up again in many countries, fears of a possible third wave of the virus, more lockdowns and curfews, and concerns over both the supply and effectiveness of vaccines.

“Flights are very full from a cargo point of view, but with no recovery in the passenger market, airline intercontinental operations are still mainly cargo-driven and they need higher prices to make these operations financially viable.”

Indeed these combinations have resulted to ‘relentlessly high’ dynamic load factors, but unfortunately higher air freight prices. Considering the volume and weight of cargo flown and capacity available, cargo load factors were 7 percentage points higher in 2019 at 73 percent for March, 8 percent up if you compare to last year or 74 percent.

Capacity for air cargo meanwhile was down 14 percent in March against 2019 but up 12 percent versus the same month last year, around the time when lockdowns were used as patchwork to mitigate the virus spread. The decline in capacity relative to 2019 should be seen, CLIVE Data notes, in the context of passenger airlines starting traditional summer schedules in March of that year—which was not the case this time around or last year.

On the Atlantic, CLIVE reports record load factors in both directions, reaching 90 percent westbound for the last two weeks of March. On eastbound sectors, for example, the Chicago (ORD) to Western Europe route reached 80 percent earlier in the month, signalling the ‘tipping point’ at which prices often increase exponentially.

“On this market, they went up by a quarter during this time frame, even though the load factor increased by ‘just’ 5 percentage points. ‘And the prices came down just as fast again when the load factor dropped below this tipping point,’” CLIVE stated.

Comparing the current China-to-Europe trade lane to 2019 shows a similar pattern at a global level: the push forward in this market seems to be decelerating. Volumes in the second week of March were 7 percent higher than in 2019, but then dropped to 6 percent and 4 percent in the following weeks.

In terms of dynamic load factor, westbound flights from China ‘still filled to the brim,’ logging 93 percent for the month. This confirms the impact of high load factors on airfreight pricing on the same route, according to TAC Index. The last three years reveal spikes of 30 percent and 17 percent, respectively, year-on-year, and more than a 50 jump versus 2019.

- March 2019: US$2.70 per kilo

- March 2020: US$3.51 per kilo

- March 2021: US$4.09 per kilo

Month on month, airfreight prices in March from London Heathrow (LHR) to North America show an increase of US$0.38 or £0.28 per kilo, up 8 percent in average pricing. Comparing 2020 over 2021, the average price in March rose €2.13 (US$2.51) per kilo, as the highest price of £4.04 or US$5.61 in week 4 reflected almost a 45 percent increase, up 400 percent if you pair with 2019.

“Pricing in March and February did not show big volatility month-over-month and, also, the intra-month volatility was not as big as in previous periods. Whether this can now be viewed as a relatively stable situation on a much higher level than in 2019 remains to be seen. It is definitely interesting to note that pricing on all lanes discussed here are higher than at the end of March 2020 when the PPE impact kicked in,” stated Robert Frei, business development director at TAC Index.

CLIVE Data Services’ first-to-market data is continuing to focus on comparing the current state of the market to pre-Covid 2019 volume, capacity and load factor data until at least Q3 of this year. This is being produced alongside the 2020 comparison.

Update: Correction on ‘reign’ to ‘rein’