Global air cargo capacity in September was 25 percent on average compared to the same month of last year (Courtesy of John Imagawa/Unsplash)

A record dynamic loadfactor and high airfreight rates on the world’s premier trade lanes in September showed the global air cargo market edging towards a sustainable recovery at the start of the traditional peak season, say leading industry analysts CLIVE Data Services and TAC Index.

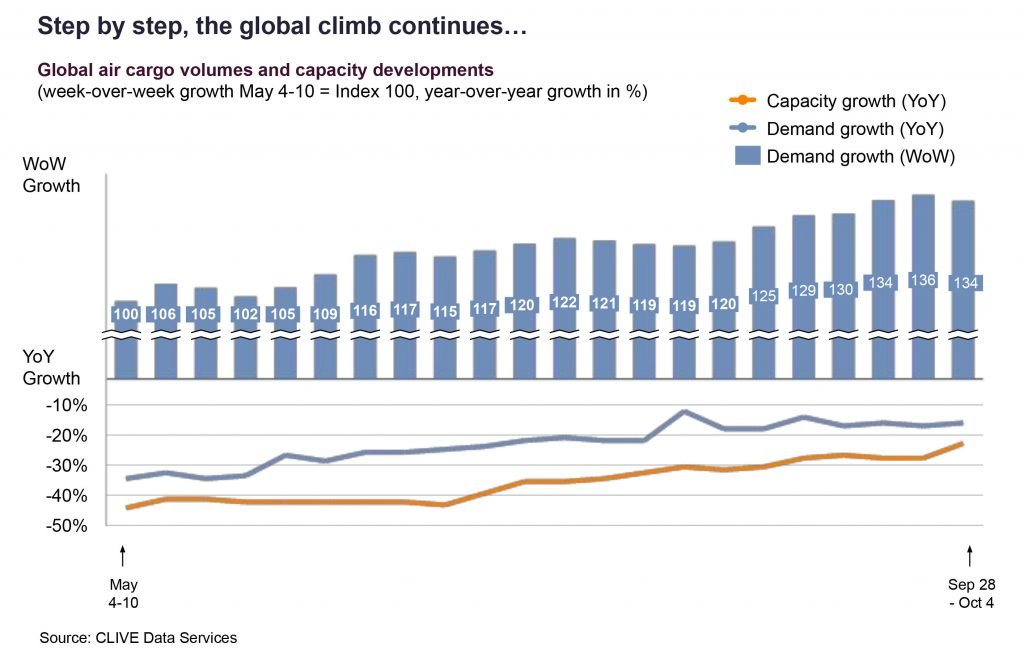

Chargeable weight in September rose 9 percentage points over last month, further narrowing the year-on-year gap to –15 percent.

This is the fifth consecutive month of positive indicators since April 2020’s 37 percent year-on-year drop in volume. CLIVE’s dynamic loadfactor— based on both the volume and weight perspectives of cargo flown and capacity available—averaged 70 percent in September, a 2 percentage points increase against August 2020 and 8 percentage points higher than last year.

Notably, the 71 percent figure for the week of Sep 28-Oct 4 was the highest ever recorded by CLIVE. Global air cargo capacity in September was, on average, 25 percent less than in the same month of last year.

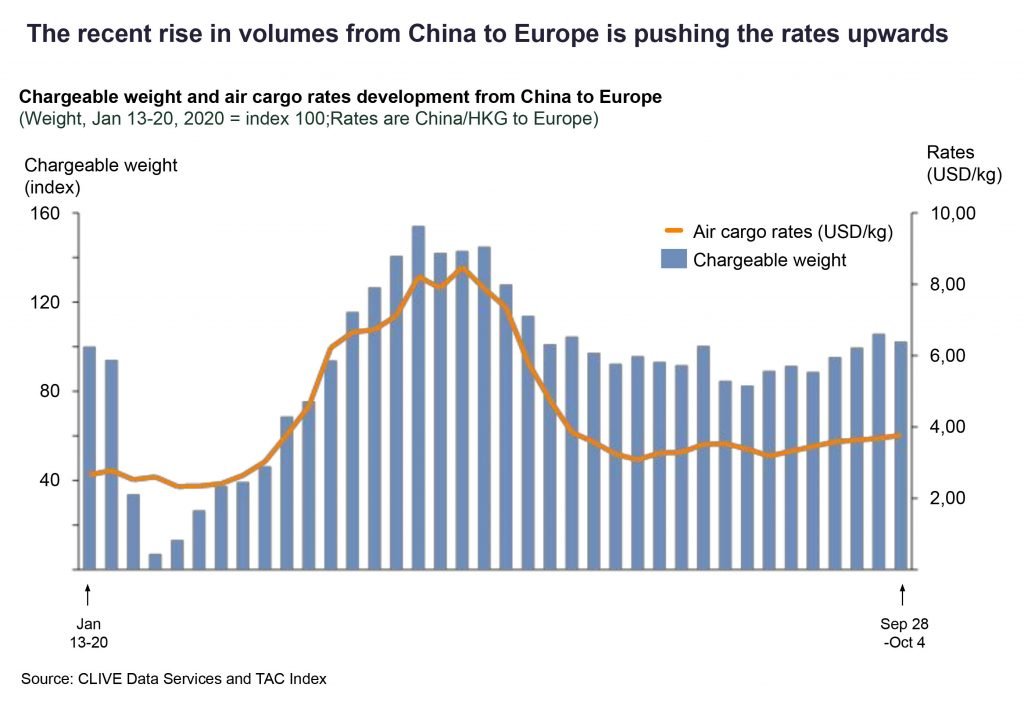

Constrained capacity in the market at a time of rising demand led to significant increases in rates, according to TAC Index. “It is interesting to see how closely demand/volume and pricing correlate in light of the fact there are a lot less BSAs (Block Space Agreements) in place currently. There were steady increases in pricing week-over-week in September, with rates on lanes from China/Hong Kong to the EU in the last week of September 8 percent higher than in the last week of August,” commented Robert Frei, business development director at TAC Index.

Latest CLIVE Data Service and TAC Index analyses of the dynamic loadfactor and airfreight rates on trans-Atlantic routes reported even higher gains. The elevated load factor for westbound volumes rose to 84 percent in September—up 18 percentage points versus September 2019—while the eastbound ‘dynamic loadfactor’ was 67 percent. Corresponding westbound and eastbound airfreight rates rose 170 percent and 73 percent, respectively, over the same period of last year.

Niall van de Wouw, managing director of CLIVE Data Services, said: “A fifth consecutive month of gradual air cargo market improvements may not be sensational news but, in this case, sometimes boring is good. In fact, our latest weekly analyses reveal more positivity than I would have expected based on the global impact of government actions to restrain the spread of COVID-19. The air cargo market seems to be quite resilient. In April, CLIVE stated that the industry’s downward performance was ‘bottoming out’ and this has proven to be correct, with month-over-month improvements ever since.

“While this might be encouraging news for airlines, it means shippers and forwarders are being faced with higher airfreight costs. Uncertainty over how the market will develop alongside very high load factors is a toxic combination for the buyers of airfreight capacity. If this demand persists, and shippers are prepared to pay, we may well see a resurgence in passenger planes being deployed mainly or solely for moving freight. These remain uncertain times but with more optimism in the market for October and November volumes, the question is: how far can the recovery go?”