Chuttersnap/Unsplash

The International Air Transport Association (IATA) announced that demand for air services is beginning to recover after hitting bottom in April. Passenger demand in April (measured in revenue passenger kilometers or RPKs), plunged 94.3 percent compared to April 2019, as the COVID-19-related travel restrictions virtually shut down domestic and international air travel. This is a rate of decline never seen in the history of IATA’s traffic series, which dates back to 1990.

More recently, figures show that daily flight totals rose 30 percent between the low point on 21 April and 27 May. This is primarily in domestic operations and off of a very low base (5.7 percent of 2019 demand). While this uptick is not significant to the global dimension of the air transport industry, it does suggest that the industry has seen the bottom of the crisis, provided there is no recurrence. In addition, it is the very first signal of aviation beginning the likely long process of re-establishing connectivity.

“April was a disaster for aviation as air travel almost entirely stopped. But April may also represent the nadir of the crisis. Flight numbers are increasing. Countries are beginning to lift mobility restrictions. And business confidence is showing improvement in key markets such as China, Germany, and the US. These are positive signs as we start to rebuild the industry from a stand-still. The initial green shoots will take time—possibly years—to mature,” said Alexandre de Juniac, IATA’s Director General and CEO.

IATA calculated that by the first week of April, governments in 75% of the markets tracked by IATA completely banned entry, while an additional 19% had limited travel restrictions or compulsory quarantine requirements for international arrivals. The initial flight increases have been concentrated in domestic markets. Data from late May show that flight levels in the Republic of Korea, China, and Vietnam have risen to a point now just 22-28% lower than a year earlier. Searches for air travel on Google also were up 25% by the end of May compared to the April low, although that’s a rise from a very low base and still 60% lower than at the start of the year.

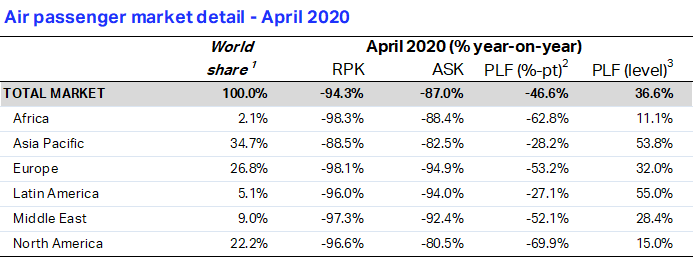

International passenger markets

April international passenger demand collapsed 98.4% compared to April 2019, a deterioration from the 58.1% decline recorded in March. Capacity fell 95.1%, and load factor plunged 55.3 percentage points to 27.5%.

Asia-Pacific airlines’ April traffic plummeted 98.0% compared to the year-ago period, worsened from a 70.2% drop in March. Capacity fell 94.9% and load factor shrank 49.9 percentage points to 31.3%.

European carriers’ April demand toppled 99.0%, a sharp decline from the 53.8% decline in March. Capacity dropped 97% and load factor shrank by 58 percentage points to 27.7%.

Middle Eastern airlines posted a 97.3% traffic contraction for April, compared with a 50.3% demand drop in March. Capacity collapsed 92.3%, and load factor crumbled to 27.9%, down 52.9% percentage points compared to the year-ago period.

North American carriers had a 98.3% traffic decline in April widened from a 54.7% decline in March. Capacity fell 94.4%, and load factor dropped 57.2 percentage points to 25.7%.

Latin American airlines experienced a 98.3% demand drop in April compared to the same month last year, from a 45.9% drop in March. Capacity fell 97.0% and load factor fell 34.5 percentage points to 48.1%, highest among the regions.

African airlines’ traffic sank 98.7% in April, nearly twice as bad as the 49.8% demand drop in March. Capacity contracted 87.7%, and load factor dived 65.3 percentage points to just 7.7% of seats filled, lowest among regions.

Domestic passenger markets

Domestic traffic fell 86.9% in April, with the steepest declines registered in Australia (-96.8 percent), Brazil (-93.1 percent), and the US (-95.7 percent). This was a sharp deterioration compared to a 51.0 percent decline in March. Domestic capacity fell 72.1 percent and load factor dropped 44.3 percentage points to 39.5 percent.

China’s carriers posted a 66.6 percent year-on-year decline in traffic in April, little changed from a 68.7% decline in March but an improvement from the 85 percent decline in February.Russian airlines’ domestic traffic fell 82.7 percent in April compared to April 2019. The slower shrinkage compared to the other markets is attributable to the later timing of the outbreaks in the country.

The bottom line

“For aviation, April was our cruelest month. Governments had to take drastic action to slow the pandemic. But that has come with the economic cost of a traumatic global recession. Airlines will be key to economic recovery. It is vital that the aviation industry is ready with bio-safety measures that passengers and air transport workers have confidence in. That’s why the speedy implementation of the International Civil Aviation Organization’s (ICAO) global guidelines for safely re-starting aviation is the top priority,” said de Juniac.

The ICAO Council’s “Takeoff: Guidance for Air Travel through the COVID-19 Public Health Crisis” is the authoritative and comprehensive framework of risk-based temporary measures for air transport operations during the COVID-19 crisis. These were developed through broad-based consultations with governments, the World Health Organization, and with key advice from aviation industry groups including IATA, Airports Council International (ACI World), the Civil Air Navigation Services Organization (CANSO), and the International Coordinating Council of Aerospace Industries Associations (ICCAIA).

“We fully support its recommendations and look forward to working with governments for a well-coordinated implementation. The world cannot afford to delay,” said de Juniac.