Courtesy of IATA

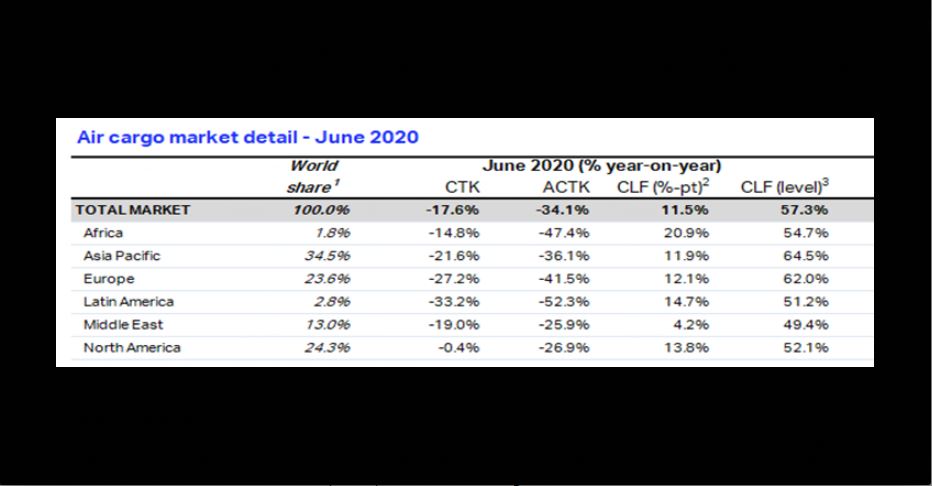

Results from the International Airport Transport Association (IATA) show that demand for air cargo in Asia Pacific fell 21.6 percent year-on-year in June, reflecting a mild improvement from the 24.6 percent drop in May, a press release confirmed. International cargo demand for the region meanwhile contracted to an even 20 percent from the 18.8 percent dip posted in the previous month.

IATA said that despite manufacturing starting to pick up in the region, the reduction in air shipments of PPE affected the demand, although key trade routes remained relatively resilient, including Asia–North America, Africa–Asia, and Europe–Asia.

“Cargo is, by far, healthier than the passenger markets but doing business remains exceptionally challenging. While economic activity is re-starting after major lockdown disruptions there has not been a major boost in demand. The rush to get personal protective equipment (PPE) to market has subsided as supply chains regularised, enabling shippers to use cheaper sea and rail options. And the capacity crunch continues because passenger operations are recovering very slowly,” said Alexandre de Juniac, IATA’s Director General and CEO.

Global demand (in cargo tonne-kilometres or CTKs) fell 17.6 percent in June (19.9 percent for international operations) compared to the previous year, showing modest improvement from the 20.1 percent YoY drop recorded in May.

Meanwhile, global capacity (in available cargo tonne-kilometres or ACTKs) shrank 34.1 percent in June (‑33.9% for international operations) compared to the previous year, on par with the 34.8 percent year-on-year drop in May.

Further, belly capacity for international air cargo shrank 70% in June compared to the previous year due to the withdrawal of passenger services amidst COVID-19, which was partially offset by a 32% rise in capacity through expanded use of freighter aircraft.

IATA said that all regions recorded declines in air cargo volume for June. The sharpest drops in year-on-year growth were posted by airlines in Europe (–27.6%) and Latin America (–29.4%), whilst carriers in Asia Pacific and the Middle East experienced 20 percent and 19.1 percent drops, respectively. North American and African saw more moderate drops compared to the other regions at 8.8% and 13.8, respectively.

All regions also saw annual contraction in international capacity, led by carriers from Africa (–46.2 percent), Latin America (–43.6%), Europe (–40.7 percent), followed by Asia Pacific (–32.3 percent), North America (–30.7 percent), and the Middle East (–25.8 percent).